Introduction

On 9 July 2025, Climate Law No. 7552 was published in the Official Gazette and entered into force immediately, establishing Türkiye’s first comprehensive climate legislation and, more importantly for the readers of this article, the legal foundation for a national Emissions Trading System.

The era of unpriced carbon in Türkiye is over.

That is not hyperbole. The TR ETS pilot phase is launching in 2026. Secondary legislation is being finalized. The Carbon Market Board has been constituted. And the EU’s Carbon Border Adjustment Mechanism has already begun imposing financial obligations on imports from countries without equivalent carbon pricing, which means Turkish exporters of steel, cement, aluminium, and fertilizers are feeling the pressure right now, as you read this.

This article is written for business executives, in house counsel, compliance officers, and operations directors who need to understand what the TR ETS means in practice: what it requires, when requirements take effect, how much noncompliance will cost, and where the strategic opportunities lie. I have tried to avoid the purely academic and focus on what matters when you are sitting in a boardroom making resource allocation decisions.

1. Legislative Background

Türkiye ratified the Paris Agreement in 2021, setting a net zero target of 2053. For several years after ratification, the practical question was: when will this commitment translate into enforceable obligations for the private sector? The answer came through a series of policy signals, starting with references to a planned ETS in the annual Medium Term Programs from 2022 onward, followed by the Long Term Strategy document (LTS 2053) presented at COP 29 in November 2024.

The Climate Law was adopted by the Grand National Assembly on 2 July 2025. It had been expected earlier in the spring session, but the government opted for additional review following feedback from industry groups. In our view, the delay was productive. The version that ultimately passed reflects a more considered approach to phasing and penalty calibration than what was circulating in draft form in early 2025.

The law was published in Official Gazette No. 32951 on 9 July 2025 and took effect the same day.

Within two weeks, on 22 July 2025, the Directorate of Climate Change published the first draft implementing regulation for public consultation, with the comment period closing on 4 August 2025. That timeline was aggressive, and it drew criticism from some industry associations who felt the window for meaningful input was too narrow. Whether or not you agree with that criticism, the pace signals the government’s determination to have the pilot operational in 2026.

2. Institutional Architecture

One of the things we tell clients early in any briefing on the TR ETS is this: you need to know not just what the rules are, but who enforces them. The Climate Law creates a multi-layered governance structure, and understanding which institution does what will save you significant time and frustration when compliance questions arise.

2.1 The Carbon Market Board

The Carbon Market Board (Karbon Piyasası Kurulu) sits at the top of the TR ETS governance structure. It is chaired by the Minister of Environment, Urbanization and Climate Change, and its members include deputy ministers from seven ministries as well as the heads of key regulatory bodies. The Board’s mandate covers the major strategic decisions: approving national allocation plans, setting the distribution of free allowances, determining offset limits, and deciding on the parameters of both the pilot and implementation phases.

In practice, this means the Carbon Market Board will be the institution that determines how much your company pays for carbon. The composition is deliberately cross-ministerial, which should help balance industrial competitiveness concerns with environmental ambition. But it also means the Board could become a venue for inter-ministerial tensions, particularly as the transition to auctioned allowances approaches.

2.2 The Directorate of Climate Change

The Directorate of Climate Change (İklim Değişikliği Başkanlığı) handles the operational side: issuing GHG emission permits, overseeing MRV processes, managing offset mechanisms, and coordinating climate policy at the national and international level. If the Carbon Market Board sets the strategy, the Directorate executes it. For most businesses, the Directorate will be the primary point of regulatory contact.

2.3 Energy Exchange Istanbul and EMRA

Energy Exchange Istanbul (EPIİAŞ, or EXIST internationally) is the designated market operator. It will organize secondary market trading, manage the national registry system for allowances, and conduct primary market auctions when those commence. The Energy Market Regulatory Authority (EMRA/EPDK) oversees market integrity, surveillance, and prevention of market abuse. For companies that have dealt with EMRA in the energy context, this institutional continuity should provide some degree of familiarity.

The key takeaway: four institutions, each with distinct roles. Know which one you are dealing with for each obligation.

3. Scope and Sectoral Coverage

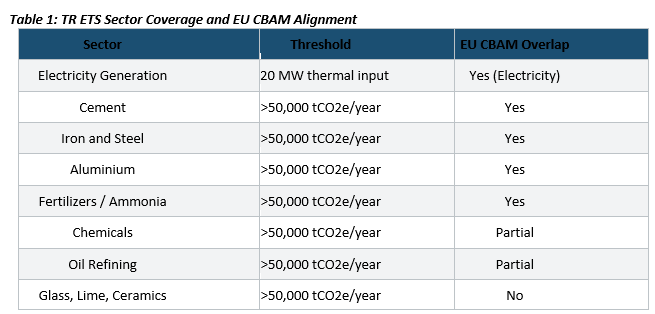

This is the section most of our clients turn to first, so let us be direct. If your facility directly causes greenhouse gas emissions and those emissions exceed 50,000 tonnes of CO2 equivalent per year, you are almost certainly within scope. The covered sectors include electricity generation (installations with a total rated thermal input of 20 MW or more), cement, iron and steel, aluminium, fertilizers and ammonia, chemicals, oil refining, glass, lime, ceramics, mineral fiber, and brick production.

The overlap with the EU CBAM is not coincidental. Türkiye’s cement exports account for nearly 30% of the EU’s total cement imports. Iron and steel represent about 9%. The TR ETS was designed, in part, to create a domestic carbon price that can be deducted from CBAM liabilities. If your sector is covered by CBAM, you can assume you will be covered by the TR ETS as well.

One important detail: Türkiye’s MRV system has been operational since 2015 and already covers roughly 770 installations. If your facility has been reporting under the existing MRV framework, the transition to ETS compliance will be less dramatic than for a facility starting from zero. But if you have been treating MRV as a box-ticking exercise, that approach will no longer suffice. The quality and accuracy of your reported data will now carry real financial consequences.

Table 1: TR ETS Sector Coverage and EU CBAM Alignment

4. The Phased Rollout: Pilot and Beyond

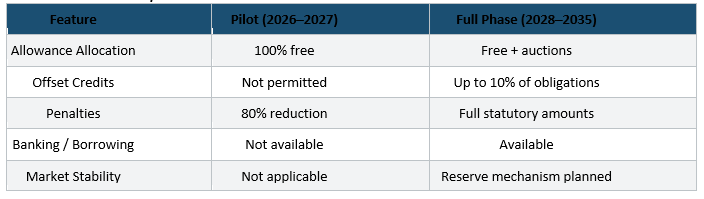

4.1 Pilot Phase (2026 to 2027)

The pilot phase is where we are right now, and it is the period that matters most for companies making decisions today. Let us walk through what it means operationally.

During the pilot, all allowances are distributed free of charge. There is no auctioning, no market price in the traditional sense, and carbon credit offsets are not permitted. Administrative penalties apply at only 20% of their full statutory levels (an 80% reduction). Entities covered by the ETS are deemed to hold temporary permits and must obtain formal GHG emission permits from the Directorate within three years of the law’s entry into force, meaning by July 2028 at the latest.

Now, we have heard some clients interpret this as meaning the pilot is essentially a rehearsal with no real teeth. That is a mistake. Even at 20% of statutory levels, the fine for failing to surrender sufficient allowances is still calculated at twice the prevailing allowance price per missing unit. The obligation to surrender additional allowances for excess emissions in the following year is fully operative. And perhaps most critically, repeated noncompliance during the pilot can lead to permit revocation, which means your facility cannot legally operate.

We advised a mid-sized cement manufacturer last autumn that approached the pilot as a “soft launch.” After reviewing their monitoring infrastructure, it became clear that they lacked the internal capacity to produce verified emissions reports to the standard required by the Directorate. Had they waited until the full implementation phase to address that gap, the consequences would have been far more costly. The pilot is the time to fix these problems.

4.2 Full Implementation (2028 to 2035)

The transition to full implementation will bring several material changes. Allowances may begin to be offered through primary market auctions, introducing an actual market price for carbon. Free allocation will continue, but based on a benchmarking methodology that rewards installations operating more efficiently than the sectoral average. Domestic offset credits will become permissible up to 10% of surrender obligations. Market stability mechanisms and allowance banking and borrowing features are expected to become operational.

The timeline is also politically significant. By 2028, the EU CBAM will be fully operational, and the gap between having a domestic carbon price and not having one will translate directly into euros for Turkish exporters. The government understands this, which is why the Pre Accession Economic Reform Program for 2026 to 2028 treats the TR ETS as a core reform measure.

Table 2: Pilot vs. Full Implementation at a Glance

5. How Allowances Work

Under the Climate Law, an allowance is a tradeable, electronically registered instrument representing the right to emit one tonne of CO2 equivalent during a specified period. Allowances are issued through the national registry and distributed either for free or through auctions.

The free allocation methodology uses a benchmarking approach at the sub-installation level. This is similar to what the EU ETS does, and the principle is straightforward: if your facility operates more efficiently than the sector benchmark, you receive more allowances than you need and can sell the surplus. If you operate less efficiently, you face a shortfall and must either reduce emissions or acquire additional allowances on the secondary market.

One restriction worth flagging: the law prohibits the use of allowances as collateral. This means you cannot pledge your allowances against a loan or use them as security for financial obligations. For companies accustomed to treating tradeable instruments as balance sheet assets, this limitation requires adjustment in financial planning.

Financial institutions and entities without compliance obligations are expected to be excluded from market participation in the initial phases. This was a deliberate policy choice to prevent speculative trading from distorting prices before the market has sufficient liquidity and depth to absorb it. Whether that restriction will hold as the market matures remains an open question.

6. Monitoring, Reporting, and Verification

If we could give one piece of advice to every facility within the TR ETS scope, it would be this: get your MRV right before you worry about anything else.

Türkiye’s MRV framework has been operational since 2015, modeled on the EU system. Approximately 770 installations already report annually. Under the TR ETS, the requirements tighten. All covered entities must prepare annual emission data reports in accordance with monitoring plans confirmed by the Directorate of Climate Change. These reports must be verified by independent third party verifiers accredited by the Turkish Accreditation Agency (TÜRKAK). Operators must maintain emissions data for at least ten years. All processes must run through the official digital platforms.

The verification requirement is not cosmetic. Verifiers will be checking the underlying data, not just the final numbers. We have seen facilities where emissions calculations relied on outdated emission factors or where fuel consumption data was estimated rather than metered. Under the current framework, these shortcomings might draw a letter from the regulator. Under the TR ETS, they can result in fines of up to 5 million Turkish Liras, the revocation of allocations, and the invalidation of offset purchases. The stakes are fundamentally different.

7. Penalties

We spend a disproportionate amount of time on this section in client meetings, because in our experience, nothing focuses corporate attention like concrete numbers. So let us lay out the penalty structure clearly.

Failure to surrender allowances: Administrative fine equal to twice the most recent allowance market price for each missing allowance, plus an obligation to surrender additional allowances covering the excess emissions in the following compliance year. In practical terms, if the market price is 100 TL per allowance and you are 10,000 allowances short, the immediate fine is 2 million TL, and you still owe the 10,000 allowances next year.

MRV violations: Administrative fines ranging from 500,000 to 5,000,000 Turkish Liras for failures related to emissions reporting, monitoring plan compliance, and verification obligations.

Operating without a permit: If your facility operates without the required GHG emission permit or after a permit has been revoked, the penalties escalate further, including potential operational restrictions that could force a temporary shutdown.

Permit revocation trigger: If a participant fails to surrender at least 80% of verified emissions for three consecutive compliance periods, the Directorate may revoke the GHG emission permit. Once revoked, no new permit is issued for three to six months. During that period, the facility cannot legally emit greenhouse gases or receive free allowances.

Escalation: All fines double upon a first repeat violation and double again for each subsequent offence within three years. This is the provision that keeps compliance officers up at night, and rightly so.

During the pilot phase, all fines are reduced by 80%. But even at the reduced rate, the financial exposure for a large emitter is far from negligible.

8. Carbon Credits and the National Offset System

The Climate Law provides for a national carbon crediting and offsetting system overseen by the Directorate of Climate Change. This is a genuinely interesting area for forward-thinking companies, because it creates opportunities that go beyond mere compliance. From 2028 onward, regulated entities may use authorized domestic offset credits to cover up to 10% of their allowance surrender obligations. Credits can be generated from projects that verifiably reduce or remove greenhouse gas emissions, such as afforestation, renewable energy deployment, industrial efficiency upgrades, and carbon capture initiatives. Project developers must register with the national offset registry within prescribed timeframes, and fraudulent or erroneous project data will result in credit invalidation.

Here is why this matters commercially. If your company invests in a verified emission reduction project, say, a waste heat recovery system at one of your plants, you may be able to generate carbon credits that can either be used to meet your own compliance obligations or sold to other regulated entities that need them. That is a new revenue stream in a market that did not exist in Türkiye twelve months ago.

The caveat: offset use is not permitted during the pilot phase. But that does not mean you should wait until 2028 to start developing projects. Credit registration takes time, verification processes must be established, and early movers will have an advantage when the market opens.

9. The EU CBAM

We deliberately placed this section after the detailed ETS analysis because the CBAM interaction is, in our assessment, the single most important strategic dimension of the TR ETS for Turkish businesses engaged in EU trade. The EU Carbon Border Adjustment Mechanism began its financial implementation phase on 1 January 2026. Under CBAM, EU importers must purchase certificates reflecting the carbon cost embedded in imported goods. The mechanism currently covers cement, steel, aluminium, fertilizers, electricity, and hydrogen. Crucially, if an equivalent carbon price has been paid in the country of origin, the EU importer may deduct that cost from the CBAM obligation.

The numbers are stark. Modeling conducted by the European Bank for Reconstruction and Development, cited in Türkiye’s Pre Accession Economic Reform Program, estimates that without a domestic ETS, the annual CBAM cost to Turkish industry would reach approximately €138 million in 2027 under a €75/tCO2 scenario. Under a €150/tCO2 scenario, those costs could climb to roughly €2.6 billion per year by 2032. Two point six billion euros. That is the cost of inaction. The TR ETS is designed to reduce that exposure significantly. Once allowance auctions commence and a meaningful domestic carbon price is established, Turkish exporters will be able to demonstrate that they have already paid a carbon cost, which can be deducted from CBAM liabilities. The government’s projections suggest CBAM related payments could drop to around €56 million in 2027 and €1.1 billion in 2032 with a functioning domestic ETS in place.

However, during the pilot phase when all allowances are free, the effective domestic carbon cost is zero. That means EU importers of Turkish goods will still have to pay the full CBAM rate for now. The benefit materializes only as the system matures and auctioning begins. Companies that plan on the assumption that CBAM relief will arrive immediately are miscalculating.

9.1 Türkiye’s Own Border Mechanism: The SKDM

Article 8 of the Climate Law also introduces the legal basis for a national carbon border adjustment mechanism, the Sınırda Karbon Düzenleme Mekanizması or SKDM. The Ministry of Trade is empowered to determine its scope, reporting requirements, and implementation. This is clearly modeled on the EU CBAM, and if implemented, it would impose carbon costs on goods imported into Türkiye from jurisdictions without equivalent carbon pricing.

For importing businesses, this is worth monitoring closely. The secondary legislation has not yet been published, but the statutory authorization is in place, and there is genuine political momentum behind it. If your supply chain includes significant imports from countries without carbon pricing regimes, you should be conducting scenario analysis now.

10. Green Finance and Revenue Allocation

The Climate Law dedicates future auction revenues exclusively to climate action and green transformation initiatives, with up to 10% earmarked for just transition measures targeting affected workers and communities. The law also promotes the development of green financial instruments, including sustainable bonds, green loans, and environmental insurance products.

A Turkish Green Taxonomy is being developed alongside the ETS framework to classify sustainable economic activities. Companies whose projects qualify under the taxonomy may benefit from preferential financing terms and access to dedicated public funds. For businesses considering capital investment in lower-emission technologies or processes, the timing of these financial incentives is designed to coincide with the ETS transition, creating a window of opportunity.

We should note that the practical impact of these financial mechanisms will depend heavily on the implementing regulations. The statutory framework is promising, but whether green finance instruments develop sufficient scale and accessibility to make a real difference for mid-market companies remains to be seen.

11. What You Should Be Doing Right Now

Let us close with the practical takeaways. Based on our advisory work with companies navigating this transition, here are the priorities we would set for any business within or potentially within the TR ETS scope.

Audit your MRV infrastructure. Not a quick review, but a genuine operational audit. Are your emission factor databases current? Is your fuel consumption data metered or estimated? Do you have staff who understand the verification process, or have you been outsourcing everything and hoping for the best? Fix gaps now, while the pilot phase penalties are still reduced.

Model your CBAM exposure. If you export to the EU in any CBAM covered sector, quantify your annual CBAM liability under multiple carbon price scenarios. Understand when the domestic carbon price will begin to offset that liability, and plan your negotiating position with EU buyers accordingly. Some EU importers are already inserting CBAM-related clauses into supply contracts with Turkish producers.

Explore offset opportunities. The 10% offset allowance post pilot may seem modest, but for a large emitter, 10% of annual surrender obligations can represent a significant volume of credits. Early investment in qualifying projects gives you both a compliance cushion and a potential trading asset.

Monitor secondary legislation closely. The Climate Law is the framework. The operational details, including benchmarking methodologies, the national allocation plan, registry procedures, and SKDM rules, will be determined through Carbon Market Board decisions, EMRA regulations, and ministerial communiqués. Companies that wait for the final rules before starting preparation will find themselves behind.

Review your supply contracts. Both as an exporter facing CBAM and as a potential importer under the future SKDM, your contractual framework needs to account for carbon costs. This includes pass-through mechanisms, reporting obligations, penalty allocation for noncompliance, and dispute resolution provisions specific to carbon regulatory requirements.

12. Final Thoughts

Climate Law No. 7552 is not a signaling exercise. It is a detailed, enforceable piece of legislation with real institutional backing, clear timelines, and penalties that escalate with each violation. The TR ETS will reshape the competitive landscape for Turkish industry over the next decade, rewarding companies that invest in emissions management and penalizing those that treat compliance as an afterthought.

The combination of domestic political commitment, EU accession alignment, and the immediate financial pressure of CBAM creates a convergence of incentives that makes delayed implementation unlikely.

The companies that thrive in this new environment will be the ones that started preparing before they were forced to. We would encourage every business within the potential scope of the TR ETS to treat the pilot phase not as a trial run, but as the beginning of a permanent shift in how Türkiye regulates industrial emissions

Let's Get Connected!